Bai Bithaman Ajil Home Financing

The Structure Of Bai Bithaman Ajil Bba House Financing Download Scientific Diagram

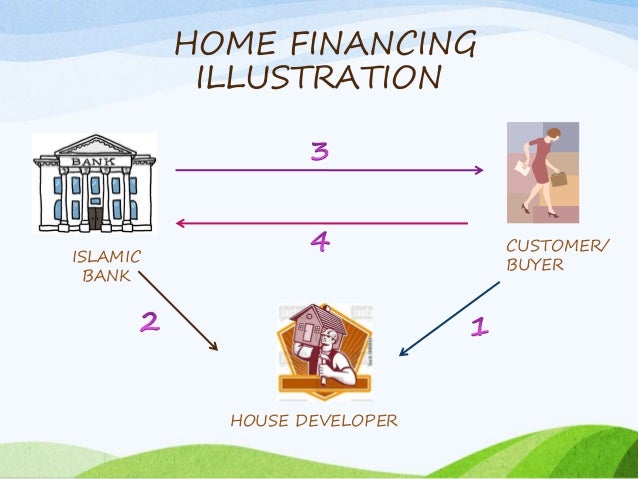

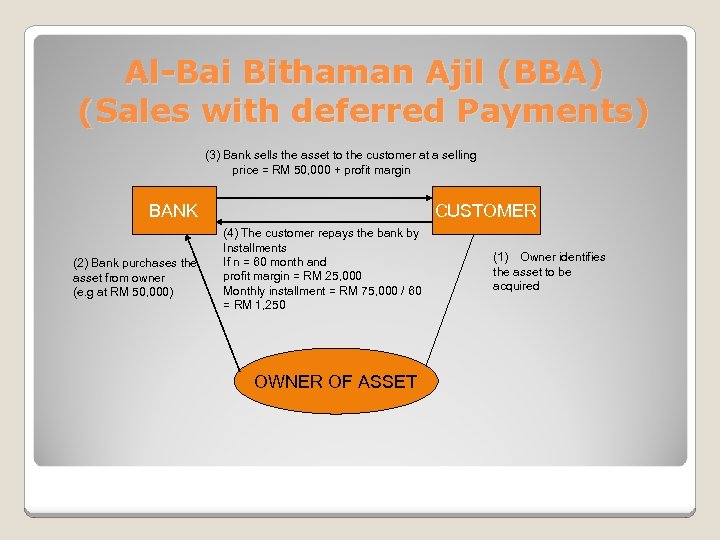

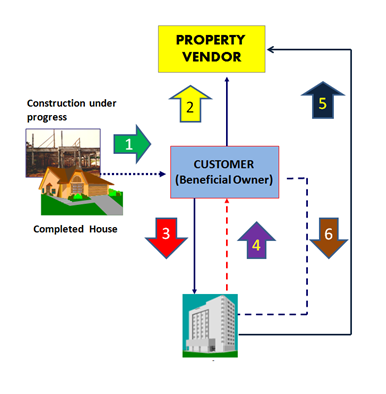

Bba Home Financing Contract Illustration Source Adapted From Bimb Download Scientific Diagram

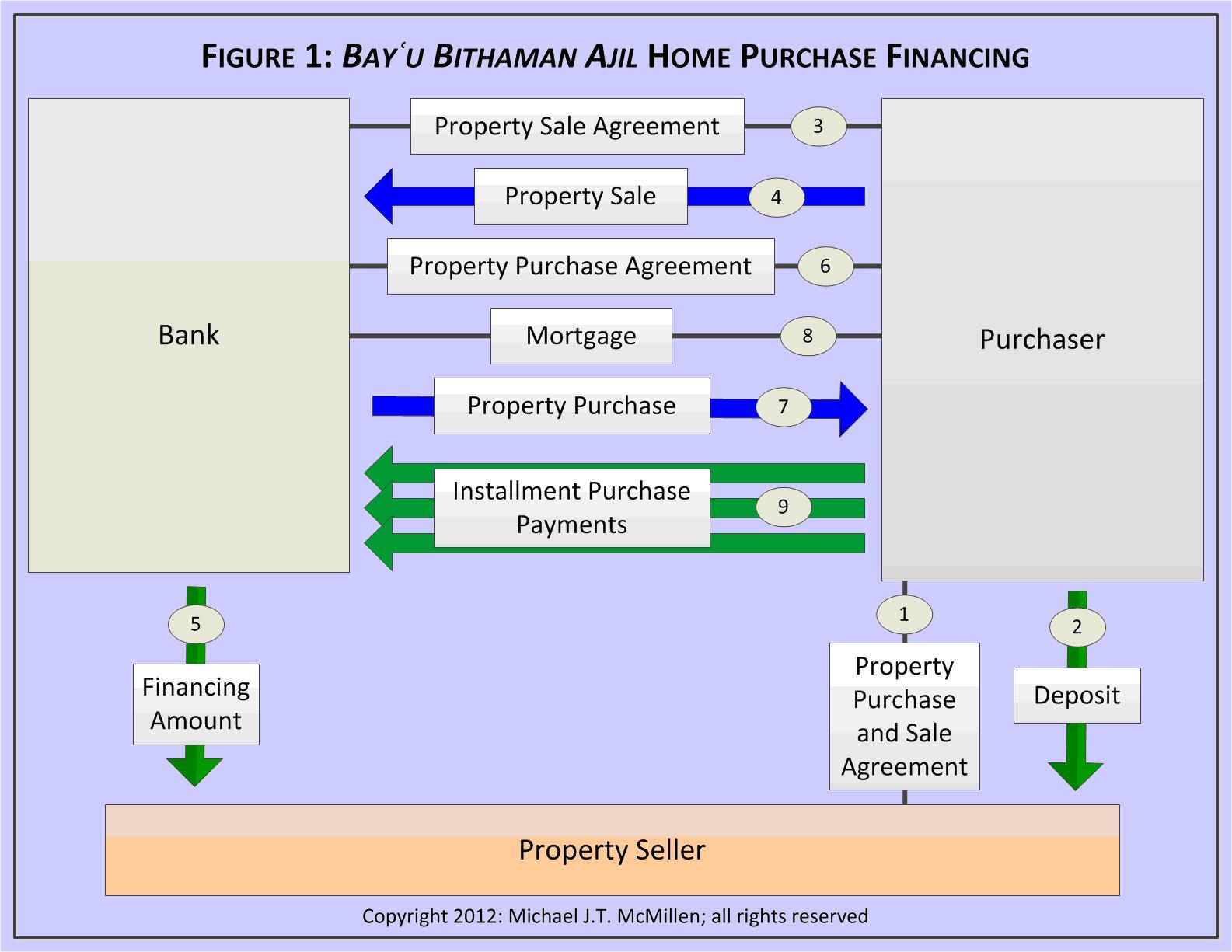

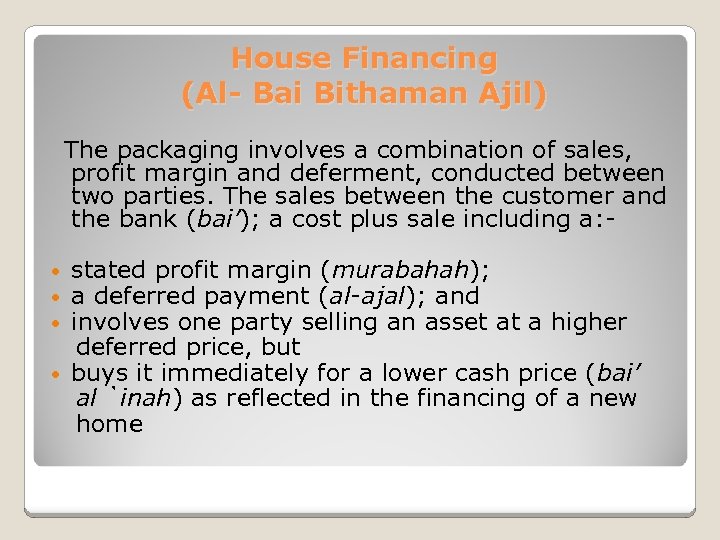

Bay Bithaman Ajil Housing Financing

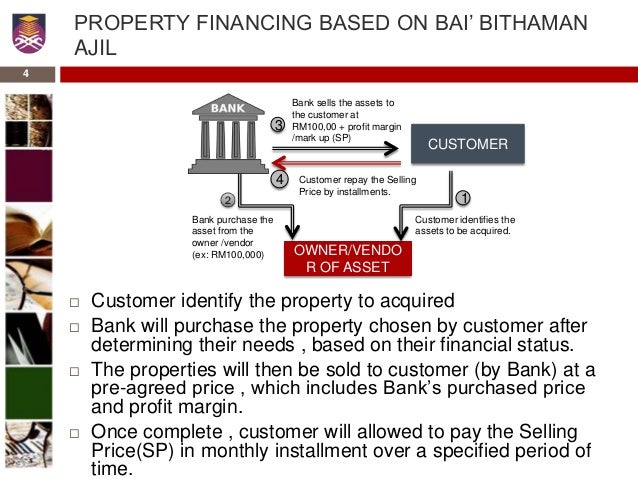

The Structure Of Bai Bithaman Ajil Bba House Financing Download Scientific Diagram

Bba Home Financing Contract Illustration Source Adapted From Bimb Download Scientific Diagram

Bay Bithaman Ajil Housing Financing

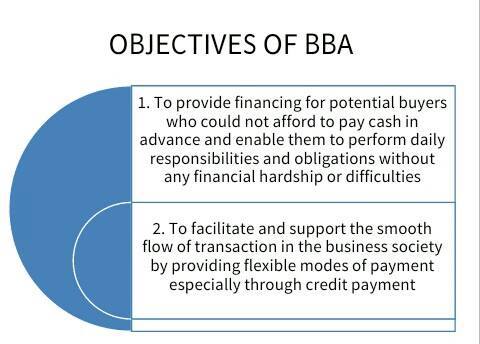

Bai bithaman ajil is one of the most popular islamic financing techniques used in malaysia and it can be considered as a substitute of the finance lease.

Bai bithaman ajil home financing. Refinancing from a conventional loan to islamic financing entitles customer to a full waiver on the stamp duty. Renovation extension of house. The current global financial crisis made some believe that the time has come for the islamic finance to assume a greater role. Islamic financial industry experienced an extraordinary growth over the last few decades and promises to grow even further.

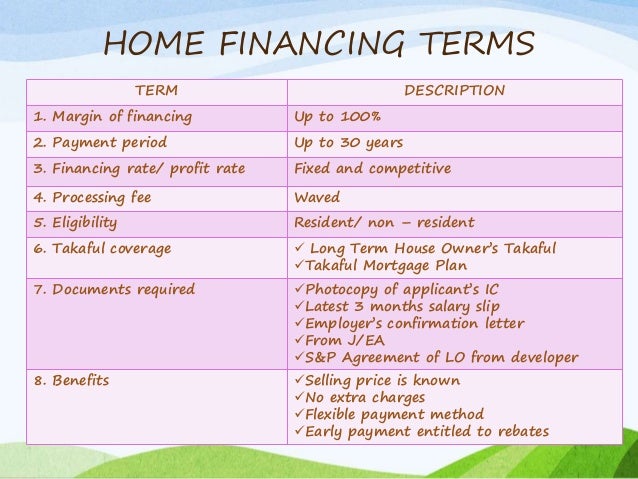

Based on the islamic principle of bai bithaman ajil bba variable rate financing allows you to finance your properties on monthly instalments that put your mind at ease and protect you from any increase in the base financing rate bfr beyond the ceiling rate. In analysing and evaluating on the application and compliance of islamic principles in al bai bithaman ajil home financing in malaysia reference will also be made to the cases referred to the. Variable rate financing is an alternative to the existing fixed rate financing. A completed home improvement financing application form.

Bai bithaman ajil bba usually bba is used for purchasing of properties home financing or commercial properties financing or sometimes for trade financing products. Rescheduling from other bank with an additional extension renovation of house. Original copy of applicant s latest three 3 months salary slips. Bai bithaman ajil bba purpose.

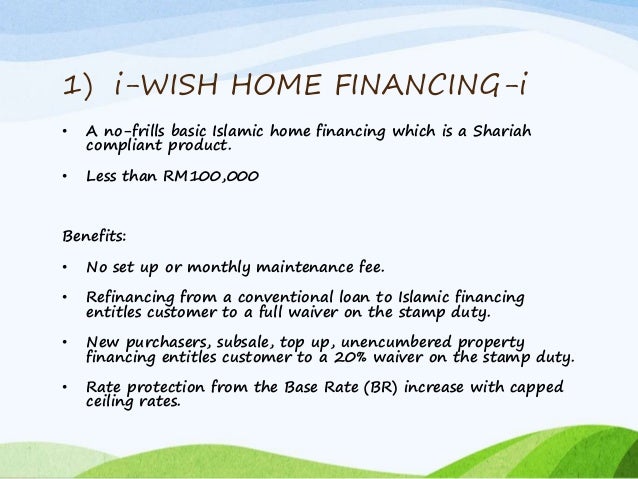

No set up or monthly maintenance fee. Identification card applicants and or home owner. It is used by customers to purchase assets of substantial value in installments from which they can generate future cash flows. Less than rm100 000 benefits.

The sale of goods on a deferred payment basis. 1 i wish home financing i a no frills basic islamic home financing which is a shariah compliant product. The dual banking system in malaysia is expected to put islamic banks at a disadvantage due to the latter s over dependency on fixed rate asset financing such as al bay bithaman ajil and murabahah when interest rates are rising rational product choice among non muslim customers nmc is expected to produce a shifting effect that may frustrate deposit mobilization and at the same time.

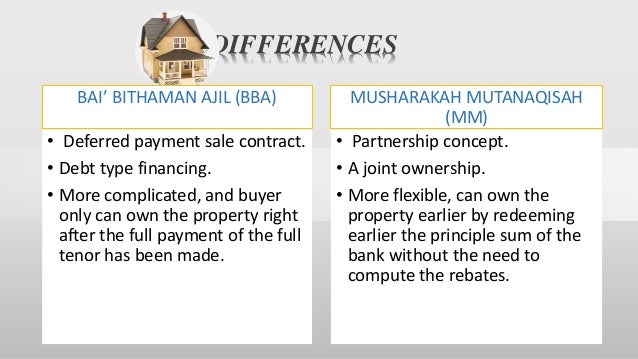

Pdf Home Financing Pricing Issues In The Bay Bithaman Ajil Bba And Musharakah Mutanaqisah Mmp Semantic Scholar

Bay Bithaman Ajil Housing Financing

Pdf Islamic House Financing Comparison Between Bai Bithamin Ajil Bba And Musharakah Mutanaqisah Mm

Pdf Home Financing Pricing Issues In The Bay Bithaman Ajil Bba And Musharakah Mutanaqisah Mmp Semantic Scholar

Islamic House Financing Bba Mm

Fundamental Of Islamic Banking Application Of Funds

Pdf Implementation Of Maqasid Shari Ah In Islamic House Financing A Study Of The Rights And Responsibilities Of Contracting Parties In Bai Bithaman Ajil And Musharakah Mutanaqisah Semantic Scholar

Ib 1005 Deposits And Financing Practices Of Islamic

Pdf Islamic House Financing Comparison Between Bai Bithamin Ajil Bba And Musharakah Mutanaqisah Mm Semantic Scholar

Pdf Consumers Acceptance On Islamic Home Financing Empirical Evidence On Bai Bithaman Ajil Bba In Malaysia Semantic Scholar

Oman Law Blog Islamic Banking

Pdf An Analysis Of House Price Index As The Alternative Pricing Benchmark For Islamic Home Financing

Ib 1005 Deposits And Financing Practices Of Islamic

Ib1005 Deposits And Financing Practices Of Islamic Financial Institutions

Ib1005 Deposits And Financing Practices Of Islamic Financial Institutions Chapter 6 Al Murabahah Bai Bithaman Ajil Property Financing Compiled By Ppt Download

Pdf A Comparative Analysis Between Musharakah Mutanaqisah And Al Bay Bithaman Ajil Contracts Under The Islamic Home Financing In Malaysia

Musyarakah Mutanaqisah An Alternatives To Bba In Home Financing

Is The Al Bai Bithaman A Jil Relatively Attractive Home Purchase Fina

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcresabj3cbumsejde8tvrtxyy9hjc1ife 4ko5flrditipi9xqs Usqp Cau

Islamic Banking Way 33a Al Bai Bithaman Ajil Principle Concepts

The Structure Of Musharakah Mutanaqisah Mm House Financing Download Scientific Diagram

Ib 1005 Deposits And Financing Practices Of Islamic

Figure Modus Operandi Of Bba Is Exhibited As Follows Download Scientific Diagram

Pdf Consumers Perception On Islamic Home Financing Empirical Evidences On Bai Bithaman Ajil Bba And Diminishing Partnership Dp In Malaysia Semantic Scholar

Bay Bithaman Ajil Housing Financing

Ib 1005 Deposits And Financing Practices Of Islamic

Islamic Financing In Practice Springerlink

Banking And Busiess Full Calculation Of Islamic Loan

Pdf Consumers Perception On Islamic Home Financing Empirical Evidences On Bai Bithaman Ajil Bba And Diminishing Partnership Dp In Malaysia Semantic Scholar

Islamic Financing In Practice Springerlink

Faq On Bai Bithaman Ajil Bba Financing

Choosing Between Islamic Home Financing Conventional Home Loan Your Home Dashboard

Pdf Consumers Acceptance On Islamic Home Financing Empirical Evidence On Bai Bithaman Ajil Bba In Malaysia Semantic Scholar